When risk-adjusted stress, holder capitulation, and cycle models align again

If you wait for Bitcoin to feel safe, you will almost always pay a premium.

Right now, 3 of the most powerful Bitcoin cycle indicators I use are lining up, and they typically appear once every 3-4 years.

When they align, the probability distribution for long-term accumulation shifts decisively.

In this article, I’m going to walk you through an institutional-grade risk metric, an on-chain signal that reveals investor psychology, and a cycle-normalised risk model.

Each tells a different story. But together, they form a coherent picture of where Bitcoin stands today.

Let’s get into it.

Risk-Adjusted Stress: The yearly Sortino dipping below zero objectively flags periods when downside volatility has overwhelmed returns, historically signalling the finest long-term entry zones for Bitcoin.

Committed Capital Underwater: When 40-50% of patient capital sits underwater, peak pessimism among committed holders creates asymmetric opportunity, with the metric now building toward that zone.

Cycle Risk In Single Digits: The Ω-Score at just 6% reflects extreme stress across multiple dimensions, marking one of the strongest historical accumulation setups.

Confluence Over Prediction: The rare alignment of technical, on-chain, and composite signals shifts probability firmly toward substantial 12-to-24-month upside for those who allocate with discipline.

The “Quality” of Risk

Let’s begin with a metric that did not originate in crypto forums, but in institutional finance.

In the TradFi world, professionals often look to the Sharpe Ratio to understand the performance of an investment relative to its risk. However, the Sharpe Ratio has a fundamental flaw when applied to an asset like Bitcoin: it treats all volatility as equal.

In the eyes of a Sharpe calculation, a 20% candle to the upside holds the same weight as a 20% collapse to the downside. For the Bitcoin investor, this is nonsensical. We don't fear the volatility of a vertical rally; we fear the volatility of a brutal drawdown. Bitcoin’s upside volatility is not a bug. It is the return profile.

The Sortino Ratio corrects this. It isolates downside volatility only. Or to put it another way, it exists to answer a simple question: how much return are you receiving per unit of downside risk?

When you calculate the Sortino Ratio over a 365-day window, something striking emerges. The most attractive long-term allocation periods in Bitcoin’s history have consistently occurred when the yearly Sortino Ratio drops below zero.

A negative yearly Sortino means that, over the prior year, downside volatility has dominated returns. In plain English, it means stress has accumulated and pain has been realised.

Historically, that is precisely when forward asymmetry improves.

In 2015, 2019, and 2022, the deep negative Sortino regimes marked accumulation windows that, in hindsight, were extraordinary. But at the time, they unsurprisingly felt uncomfortable. That is the point. Risk-adjusted stress is not a headline event. It is a statistical condition.

Since late January, as Bitcoin dipped below the $80,000 mark, the yearly Sortino turned negative again. I do not treat this as a signal to perfectly time a bottom. That is fantasy. Markets are not designed to reward precision; they are designed to shake it out of you.

Instead, I treat negative Sortino territory as the opening of an allocation window. This is where disciplined dollar-cost averaging, in my eyes, becomes extremely rational. The objective is not to capture the exact low. The objective is to accumulate during regimes where downside has already been realised and the forward skew historically tilts upward.

Perfection is unnecessary when there is this level of asymmetry.

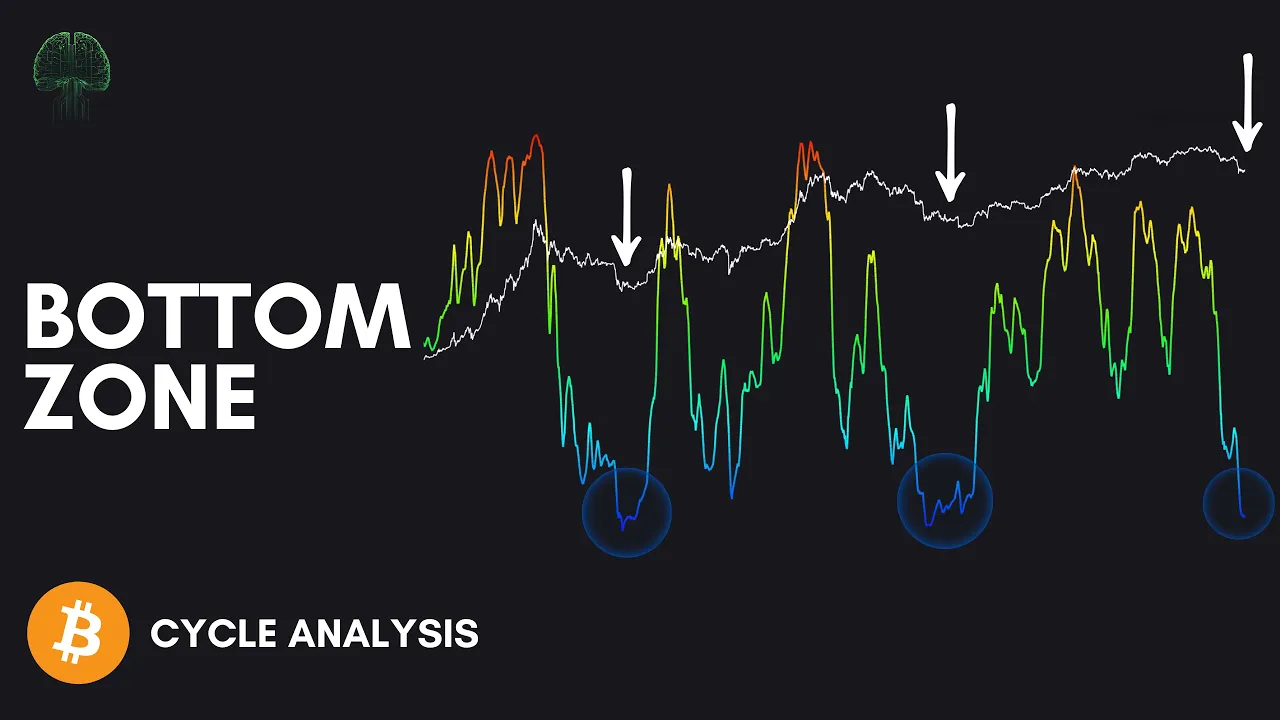

Bitcoin 365D Sortino Ratio

"Diamond Hand" Psychology

Now we move into something traditional finance cannot replicate.

What makes Bitcoin truly revolutionary from an analytical perspective is the ability to look inside the network and see exactly how different cohorts of investors are behaving. We can distinguish between the short-term speculators, who often exit at the first sign of trouble, and the Long-Term Holders (LTHs), defined as those who have held their coins for at least 5 months.

By monitoring the Long-Term Holder % Supply in Loss, we gain a direct window into the psychological state of the network’s most committed capital.

There is a fascinating trend here:

In 2015, roughly 50% of long-term holder supply was in loss near the cycle bottom.

In 2019, the peak was closer to 45%.

In 2022, it was around 40%.

We can see quite clearly that each cycle’s peak stress level declines by approximately 5%. But this isn’t a coincidence. As the asset matures and early adopters sit on lower and lower cost bases, the percentage of the long-term cohort that can be pushed underwater naturally shrinks.

Someone who accumulated meaningfully in 2017 may have been underwater in 2019, but by 2025 the probability of them being in loss is basically negligible. It proves that time is the ultimate advantage with this asset.

Currently, this metric sits around 27% and is climbing every day toward the expected 35% bottom range. That suggests we are not yet at historical peak pessimism, but we are clearly entering bottom-formation territory.

But here is the nuance that many miss: this metric doesn't just rise because the price falls. It can rise simply because of the passage of time. If an investor purchased Bitcoin 5 months ago near $115,000 and has held through the drawdown, they now find themselves "graduating” into long-term holder status. If they are still holding through this drawdown and price remains below their entry, their supply adds to this supply in loss figure.

This "time-based capitulation" is often just as important as "price-based capitulation”. It signals a market that is grinding out the weak hands and transferring wealth to those with the patience to wait for the cycle to turn.

Traditional assets cannot offer this time-based data. Equity markets cannot tell you how many long-term holders are underwater with this precision. Bitcoin can.

And that information matters when you are trying to identify psychological capitulation rather than merely price weakness.

LTH % Supply In Loss

A Confluence of Macro and Math

The final layer I want to highlight is the Ω-Score. For those unfamiliar, you can think of it as a single lens that brings together multiple perspectives: technical indicators, on-chain metrics, and macroeconomic data into a 0-100 risk score.

Bitcoin in 2013 was not Bitcoin in 2025. A tenfold price move then had very different liquidity, adoption, and macro implications compared to today. Comparing absolute values of many of your favourite indicators across cycles can be misleading; what matters is where we are relative to the cycle we’re in.

The new framework we developed for the Ω-Score accounts for the diminishing returns as the network matures, while still reflecting the extremes of investor psychology: euphoria, complacency, stress, and capitulation.

The goal isn’t to predict the next week’s candle. It’s to identify market regimes where forward returns over 12-24 months have historically been heavily skewed to the upside.

Any reading below 20% represents a zone of extreme opportunity. So to see the score drop from 20% down to 6%, as it has recently done, is a rare event. It represents a massive collapse in risk in a very short window of time.

Markets are not deterministic; there are no guarantees. But they are probabilistic. So when you have the Sortino Ratio in a negative nosedive, long-term holders feeling the squeeze, and the Omega Score deep in the single digits, the probability distribution shifts heavily in our favour.

The Bitcoin Ω-Score

The Discipline of Discomfort (Plus, What I'm Doing)

As I reflect on these signals lining up once again, I cannot help but feel a deep sense of familiarity mixed with genuine excitement (sad, I know).

Here is the uncomfortable reality: the crowd appears at the peaks, because that’s when it feels safe. When price is accelerating vertically and headlines are positive, participation feels right. Risk, however, is highest when comfort is everywhere.

The disciplined investor shows up during discomfort.

When these risk-adjusted metrics are starting to trend deep into the blue and the news is betting on the next WW3, every fibre of your lizard brain tells you to wait. It tells you to stay on the sidelines until things "clear up" or until the price starts moving back toward all-time highs.

What I am doing is turning my dollar-cost-averaging programme to its most aggressive setting and committing fresh capital steadily throughout this regime. I was very content allocating at the risk levels from 3 months ago. I am now extremely content allocating at these current risk levels.

Asymmetry does not mean certainty. It means favourable skew in the 12-24 months ahead. It means the potential upside over the next few years meaningfully outweighs the realised downside that has already been absorbed.

A few years from now, when charts are inevitably redrawn with the clarity of hindsight and commentators declare the accumulation zone “obvious”, it will not have felt obvious in real time. It will have felt uncomfortable. It will have required conviction.

So if you have read this far, you are already operating with a different mindset from the majority. Your edge is behavioural as much as it is analytical.

Bitcoin’s cycles will continue to mature. Returns will likely compress over decades. But human psychology does not evolve as quickly as technology. Fear and euphoria still oscillate. Stress still builds and releases. Capitulation still creates opportunity.

The window is open. The rest, as always, is up to us.

I’ll catch you in the next one.

Cheers,